“U.S. stocks end 2025 near record highs” was a common headline at last year’s end, yet many households and small businesses experienced something very different. Inflation remained persistent, tariffs weighed on costs, and a weakening U.S. dollar made everyday expenses feel heavier. For many Americans, growth in the markets did not translate into relief at the grocery store or confidence in their monthly cash flow.

That disconnect can feel frustrating, but it is not a contradiction. It is a reflection of how Main Street and Wall Street operate on different timelines and respond to different pressures.

As we discussed in our Carlson Quarterly – Q4 2025 update, market performance often reflects expectations about the future rather than current economic conditions. Those expectations do not always align with what people are experiencing day to day.

Two Systems, Two Timelines

Main Street and Wall Street are closely connected, but they operate on different timelines and respond to different forces.

Main Street reflects households, workers, small and mid-sized businesses, and local communities. It is driven by employment, wages, production, pricing, and access to credit. This is where income is earned, expenses are paid, and financial pressure or relief is felt in real time.

Wall Street, by contrast, is a pricing engine. It represents public markets, financial institutions, and large pools of capital that focus on expectations, valuations, liquidity, and returns. Markets translate assumptions about future growth, interest rates, earnings, and policy into today’s asset prices, often well before those changes show up in the broader economy.

Because of this, the two systems can send very different signals at the same time. Markets may look optimistic while households feel constrained by inflation, borrowing costs, or housing affordability. Understanding that difference helps explain why strong market performance does not always align with everyday economic experience.

How the Cycle Really Works

There is a constant feedback loop between Main Street and Wall Street.

Households and businesses save through retirement plans, pensions, and investment accounts. Those savings fund capital markets. In turn, capital markets provide credit and equity financing that support business growth, hiring, and innovation. Over time, that growth creates more income and more savings.

When this cycle slows or breaks down due to tight lending conditions, rising delinquencies, or sharp shifts toward risk avoidance, recessions tend to follow.

Why Markets Often Recover First

Financial markets are forward looking. They tend to bottom and recover before the broader economy improves due to increased policy support or lower interest rates.

Large public indexes are dominated by multinational companies with strong balance sheets and global revenue streams. Main Street, by contrast, is more local, more labor intensive, and far more sensitive to borrowing costs.

Policy often flows through markets first as expectations reset and reaches households and small businesses later. That timing gap helps explain why markets can rise alongside real economic strain.

History Offers Clear Examples

This unevenness is not new.

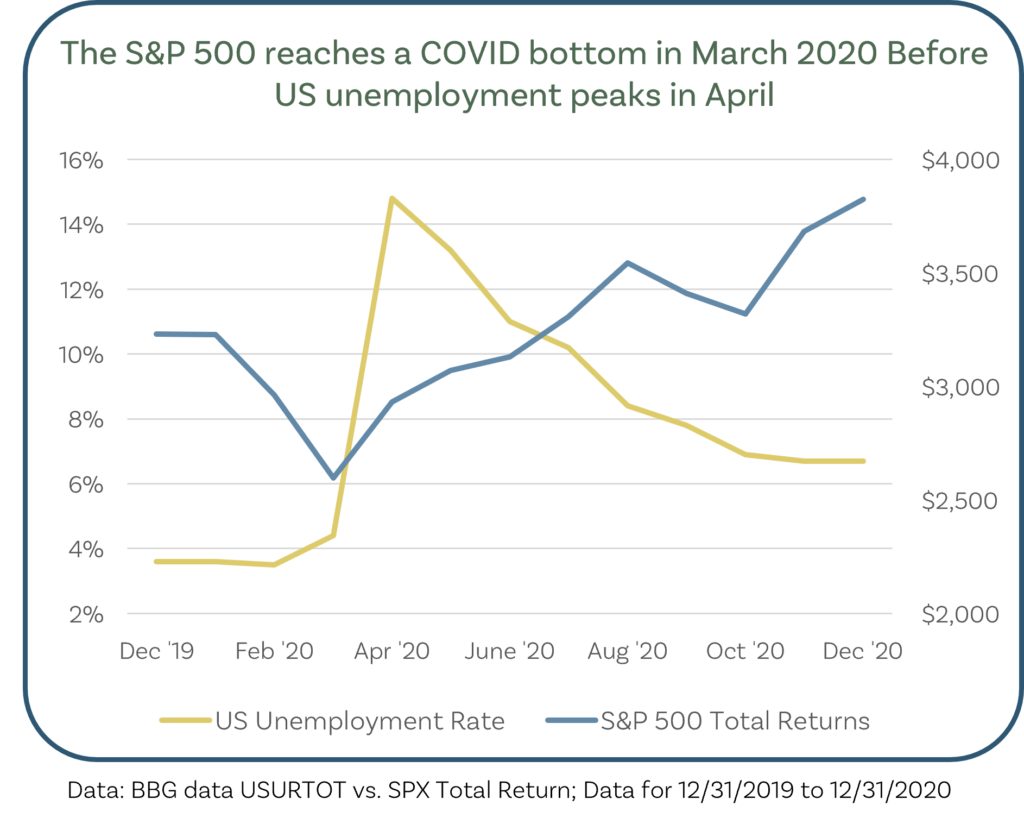

Post-COVID recovery in 2020

Markets rebounded quickly on unprecedented policy support and reopening expectations, while many households faced layoffs, closures, and a slower recovery. U.S. unemployment peaked around 8% in 2020, according to the U.S. Bureau of Labor Statistics, even as the S&P 500 finished the year up roughly 18% after an early year drawdown.

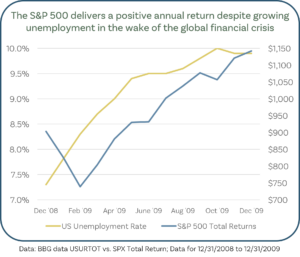

Global Financial Crisis in 2008 – 2009

Markets began stabilizing before labor markets and housing conditions fully healed. Credit remained tight, and many small businesses and households experienced a long repair cycle even as asset prices recovered.

Where the Two Worlds Overlap

Main Street and Wall Street converge when policy, prices, and credit conditions directly affect daily life. Housing affordability, wage growth, inflation trends, and borrowing conditions are where the overlap is most visible.

These are often the areas that matter most for financial planning decisions.

Choosing the Right Lens

Understanding the difference between Main Street and Wall Street helps ensure you are watching the right scoreboard for the decision in front of you.

- Investors can use markets for forward-looking signals, while using Main Street data as a reality check.

- Business owners should plan around credit availability and labor costs, not index performance.

- Households benefit from separating short-term market noise from long-term planning, maintaining disciplined savings and spending habits, and managing debt thoughtfully.

Read our article Keeping Your Financial Team Aligned and Your Plan on Track to learn more about how coordinated planning helps maintain discipline when headlines oversimplify reality.

Bringing It All Together

Main Street and Wall Street diverge because they do different jobs and move on different timelines, even though they remain deeply connected. When you understand how each system works, it becomes easier to hold two truths at once. Markets can rise while life feels hard, and everyday conditions can improve while markets remain cautious.

Clarity comes from context, not headlines. If you would like to talk through how these dynamics apply to your own situation, you can start a conversation with our team by reaching out through our contact page.

Carlson Investments does not provide tax, legal, or accounting advice. This content has been written for informational purposes only. Always consult your individual tax, legal, or financial professionals for advice tailored to your situation.

Let's Talk

Finding a better way doesn’t start with you learning about investment strategy. It starts with us learning about you.

Let’s get started.

Contact Us