When the SECURE 2.0 Act became law in 2022, it introduced dozens of changes designed to help Americans save more effectively for retirement. Several of those provisions are just now taking effect, making this a good time to revisit what the updates mean for your financial planning.

From higher contribution limits to expanded Roth options and new flexibility for younger savers, SECURE 2.0 creates opportunities across multiple stages of life.

Higher Retirement Contribution Limits

One of the law’s primary goals is to help individuals increase retirement savings as they approach retirement.

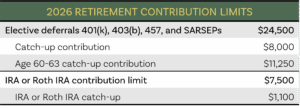

Catch-up contributions for those aged 50 and older have been available for years. As of 2025, individuals ages 60 to 63 can make an even larger catch-up contribution to employer-sponsored plans such as 401(k), 403(b), 457, and SARSEP plans.

Catch-up contributions for those aged 50 and older have been available for years. As of 2025, individuals ages 60 to 63 can make an even larger catch-up contribution to employer-sponsored plans such as 401(k), 403(b), 457, and SARSEP plans.

For 2026:

- Ages 50–59 can contribute up to $8,000 in catch-up contributions

- Ages 60–63 can contribute up to $11,250

Traditional and Roth IRA contribution limits have also increased to $7,500, with an additional $1,100 catch-up contribution for those aged 50 or older.

Contribution limits often rise over time with inflation, which means reviewing them regularly can help ensure you are maximizing your savings opportunities.

A New Rule for High Earners

Beginning in 2026, individuals earning more than $150,000 in the prior year must make any catch-up contributions to workplace retirement plans as Roth contributions.

While these contributions are made with after-tax dollars and do not reduce current taxable income, the funds grow tax free and qualified withdrawals in retirement are also tax free. For some savers, this change may provide access to Roth savings opportunities that would otherwise be limited by Roth IRA income thresholds.

For a refresher on the differences between 401(k) account types, visit our article on Understanding Your 401(k) Choices: Traditional vs. Roth, which explores how each approach can play a role in long-term planning.

Expanded Roth Options

SECURE 2.0 also broadened Roth opportunities inside employer plans.

Employers can now offer Roth matching contributions, giving employees the option to receive employer matches in a Roth account rather than a pre-tax account.

Another key change is that as of 2024 Roth funds in employer-sponsored plans are no longer subject to Required Minimum Distributions (RMDs), giving retirees more control over when they withdraw those funds.

Changes to Required Minimum Distributions

The law also increased the age when retirees must begin taking required withdrawals from retirement accounts.

The law also increased the age when retirees must begin taking required withdrawals from retirement accounts.

The RMD age increased to 73 in 2023 and will rise again to 75 in 2033.

If you turn 73 in 2026, you may delay your first RMD until April 1, 2027. However, you would still need to take your 2027 RMD by the end of that year, which could result in two withdrawals in the same tax year.

Expanded Charitable Giving Options

The SECURE 2.0 Act also expanded opportunities for Qualified Charitable Distributions (QCDs).

Individuals aged 70½ or older can donate directly from their IRA to a qualifying charity, reducing taxable income while also counting toward an RMD.

Beginning in 2026, the QCD limit increases to $111,000 annually, with a $55,000 limit for certain one-time charitable gifts.

QCDs can now also fund charitable remainder trusts and charitable gift annuities, creating additional options for individuals who want to incorporate philanthropy into their financial plans.

You can learn more about charitable planning strategies in our article Using Your Time & Resources for Good: 11 Ways to Donate to Charity.

New Flexibility for Younger Savers

SECURE 2.0 also includes provisions aimed at helping younger investors manage competing financial priorities.

Unused funds in a 529 education savings plan can now be transferred to a Roth IRA for the same beneficiary after the account has been open for 15 years. Transfers are subject to annual Roth contribution limits with a lifetime cap of $35,000.

The law also allows employers to match employee student loan payments with retirement plan contributions, helping workers make progress on both debt repayment and retirement savings.

Additionally, some retirement plans will allow employees to access certain Roth contributions for emergency expenses without penalties. This is intended to help workers build both retirement savings and an emergency cushion at the same time.

According to Bankrate, nearly 3 in 10 Americans have more credit card debt than emergency savings.

Staying Current on Retirement Rules

SECURE 2.0 introduced a wide range of changes, and additional updates will continue to take effect over the coming years. Because retirement and tax rules evolve regularly, reviewing your plan periodically can help ensure you are taking advantage of the opportunities available.

If you would like to discuss how these changes may affect your financial strategy, start a conversation with our team by reaching out through our contact page.

Carlson Investments does not provide tax, legal, or accounting advice. This content has been written for informational purposes only. Always consult your individual tax, legal, or financial professionals for advice tailored to your situation

Let's Talk

Finding a better way doesn’t start with you learning about investment strategy. It starts with us learning about you.

Let’s get started.

Contact Us