Understanding the return expectations that equity investors require from their risk assets is essential. Regardless of a company’s capitalization size or a portfolio manager’s mandate, investors want to be paid fairly for the level of risk they are willing to assume. All Cap equity portfolios can provide the return consistency and outcome dependability that many investors prefer. History teaches us that in any given year the market will favor one particular style or cap box over the others. Actively managed All Cap equity strategies can escape this fate by investing in carefully-vetted opportunities and by remaining cap and style agnostic.

Investing across the capitalization range spectrum can provide safer (less risky) outcomes over the long-term.

The key to All Cap investment success is in identifying the most attractive opportunities available in the market. This is highly-dependent upon a manager’s research capabilities; a manager that can identify the “macro” investment themes as well as the “bottom-up” opportunities. Success in All Cap investing can be fleeting if the strength of the research process is not robust or if risk in the portfolio construction process is overlooked. At D.L. Carlson, our successful All Cap portfolio includes our highest-conviction ideas derived from our proprietary research. We thoughtfully analyze the risk/return attributes of every holding, as well as the overall risk profile of the entire portfolio. If our research uncovers an attractive, compelling idea, we want that opportunity included in our portfolio despite arbitrary cap-range constraints. At the portfolio level, it’s desirable to construct an asymmetrical risk profile that is tilted in favor of generating consistently higher risk-adjusted returns. The companies in our All Cap equity strategy have sustainable competitive advantages, are well-managed, and offer meaningful appreciation potential. Our goal is to build a portfolio of these stocks that will generate substantial gains over time while providing diversification benefits to mitigate risk.

Advantages of an all cap equity portfolio strategy

- Being market cap agnostic allows a manager to pick their best research-driven ideas and not be limited to a narrower, cap-constrained group of stocks. An All Cap portfolio can include names sourced from a less-efficient and more opportunistic universe where analyst coverage is not as broad. This leads to a meaningful information advantage benefit for active management in the All Cap area.

- As conviction in an investment thesis builds, an All Cap manager is able to choose the best risk/reward opportunity that expresses the investment thesis. This expands the scope of the thematic opportunity set while also reducing company-specific risk. For example, analyzing different companies involved in the supply chain of production is a way of participating in the growth opportunity while also diversifying company-specific risk factors.

- An All Cap strategy gives the investor an efficient “one stop shop” for U.S. equities in a well-diversified, straight-forward portfolio. This helps reduce the overall management fee paid by the investor. It can also eliminate potential overlap in holdings across different portfolios which may be unintentionally risky.

- An All Cap Equity mandate allows the manager to be agile and adapt to market conditions. Market volatility can be dramatic; the ability to make portfolio decisions across the capitalization range, and rebalance risk across positions, industry sectors and/or investment themes can be done quickly (and potentially with greater tax-efficiency for taxable accounts).

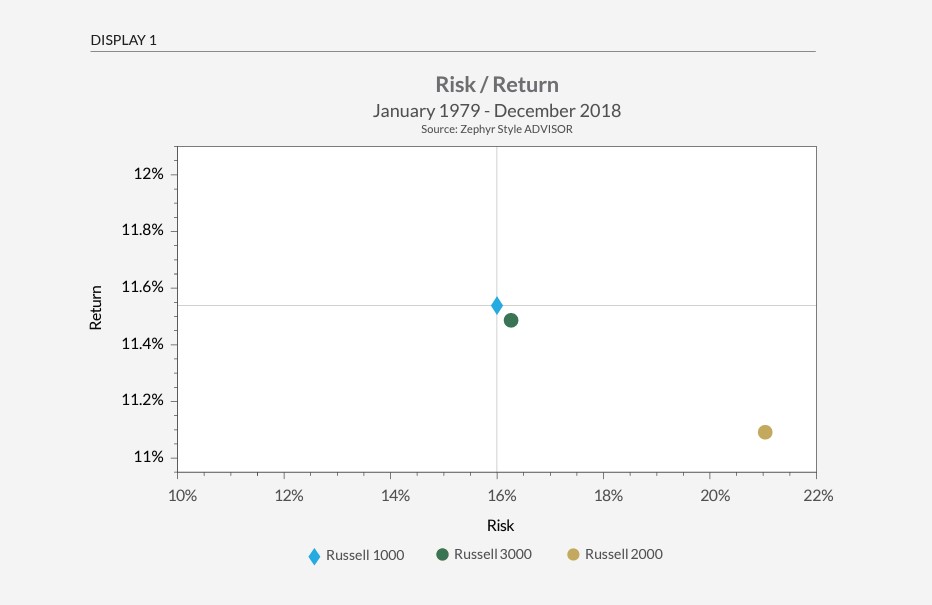

- All Cap Equity, which is typically benchmarked to the Russell 3000 index, offers a desirable balance that incorporates the higher expected long-term risk/return potential of small caps with the stability (but typically slower growth) of large caps (see Display 1).

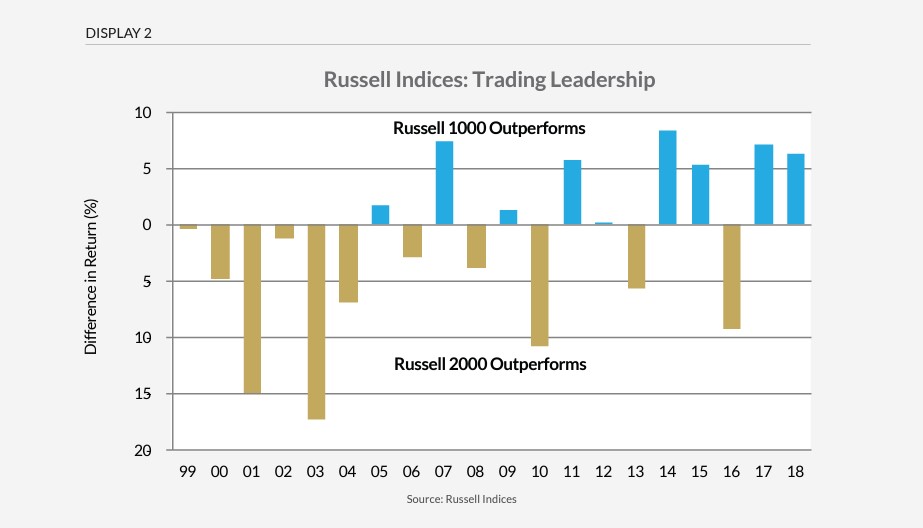

- Over the past two decades, the performance of the Russell 1000 and Russell 2000 indices have traded leadership almost equally (see Display 2) and by considerable amounts as measured by calendar year time periods. Notably, there was a meaningful streak of small cap outperformance for six consecutive years from 1999 through 2004, but neither of the two benchmarks have produced lengthy dominance over the past 14 years.

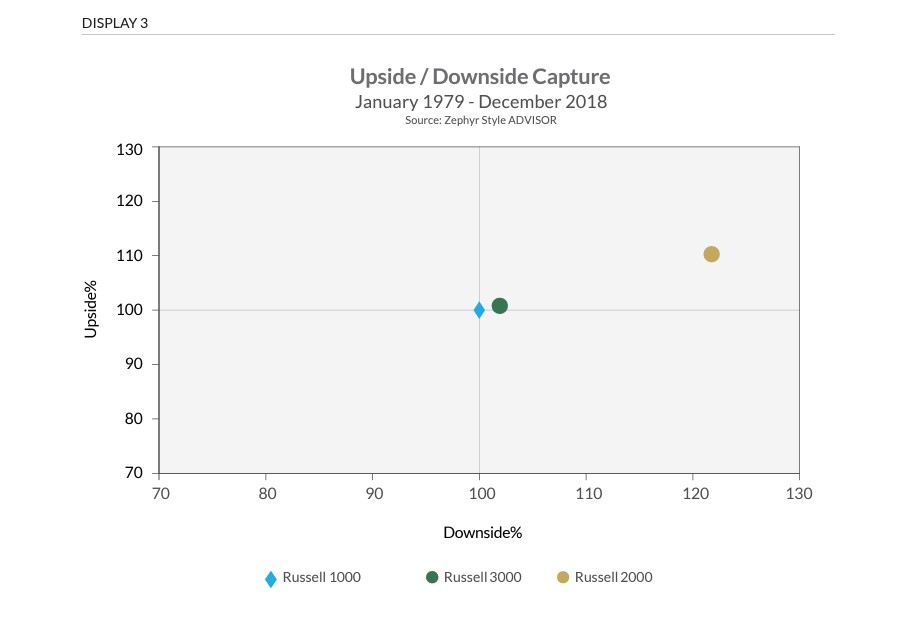

- All Cap portfolios offer the potential for more consistent long-term returns, even with a significant weight to small cap positions (see Display 3). The client experience can be better managed in terms of performance expectations.

"Market leadership is changing all the time. One of DLC's All Cap Equity strategy's most important sources of alpha is having the flexibility to capitalize on those changes."

- Jay Mullins,

CIO/President

UNDERSTANDING THE RISK PROFILE OF AN ALL CAP EQUITY STRATEGY

To better understand the compelling attributes of an All-Cap strategy, we analyzed the widely-followed Russell U.S. Equity indexes, which capture the entire U.S. stock market ranging from mega–cap to micro-cap companies. The Russell 3000 is the appropriate “best fit” benchmark for a U.S. All-Cap Equity strategy.

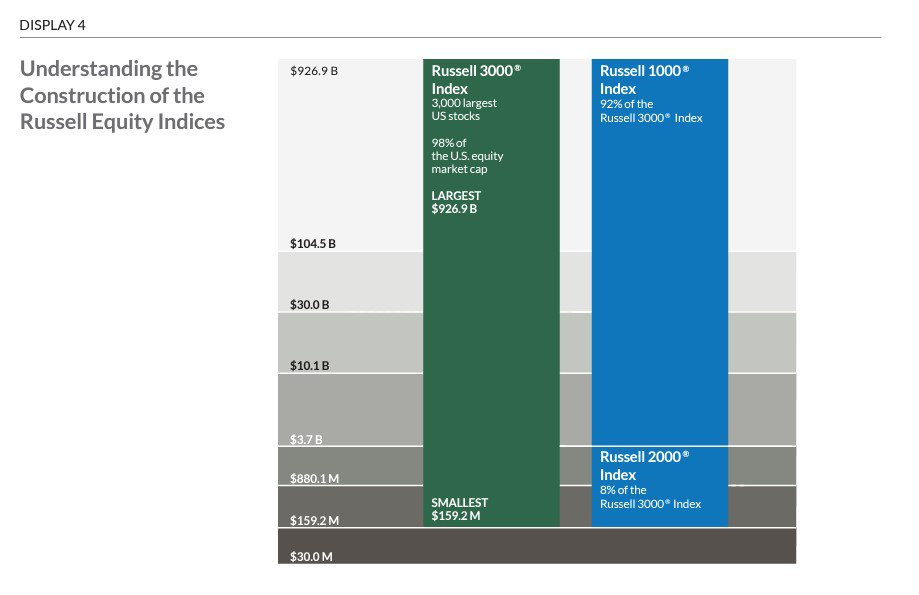

The Russell benchmarks utilize a modular index construction methodology and capture historical performance across market segments. The Russell 1000 and 2000 sub-indexes “roll-up” to create the Russell 3000 Index with no gaps or overlaps.

The Russell 1000 covers the largest 1000 stocks as measured by each company’s market cap, the Russell 2000 includes the next 2000 stocks, mostly in the small and mid-cap opportunity set. The comprehensive Russell 3000 index covers approx. 98% of the investable U.S. equity universe (see Display 4).

As depicted in Display 2, the returns of the R1000 and R2000 indices have shifted in and out of favor over time, depending on many different drivers impacting the economy and capital markets. Over the long-term, there is a smoothing of these favorable periods, and the longer term returns mean revert. When doing any type of time period return analysis, attention needs to be paid to beginning and end-point sensitivity before making any conclusions on index performance data. Slight adjustments to the beginning or ending data points can make a substantial difference in the results.

Because the magnitude of the shifts in and out of favor can be dramatic, the longer–term risk/reward profile of the R3000 provides more consistency than its components. At any point in time, a “snapshot” comparison of the R1000 and R2000 index can reflect meaningful differences in the attributes of the core components. This “real world” scenario of investing suggests that an experienced, research-driven all-cap manager can potentially add value through dynamic allocation decisions.

ABOUT CARLSON

D.L. Carlson Investment Group, Inc. is a Registered Investment Adviser with offices in Concord, NH. The firm was founded in 1989 and remains 100% employee owned. The goal of the firm’s proprietary research process is to deliver consistently high risk-adjusted returns across market cycles. The firm’s track record is GIPS verified and the team takes ownership in providing outstanding client service.

Let's Talk

Finding a better way doesn’t start with you learning about investment strategy. It starts with us learning about you.

Let’s get started.

Contact Us